In an interview today on CNBC Warren Buffett said he couldn’t find someone to come to the annual meeting to explain their position against Berkshire Hathaway going forward. He wants a big short to come in and explain the bear case. But this strikes me as a common case of bad benchmarking (and frankly, a layup to make Buffett look good since the odds are heavily in his favor).

Buffett shouldn’t be asking for someone to explain why his firm will do poorly in the future. He should be asking for someone to come in and explain why anyone should own Berkshire Hathaway relative to a highly correlated index like the S&P 500. In this manner, owning a long only alternative is similar to being bearish on Berkshire in that you believe the highly correlated index will outperform his firm.

I think there’s a pretty strong case going forward that Berkshire likely won’t outperform the S&P 500. Among the more basic arguments:

- Berkshrie has become so large that it is becoming, by definition, a huge part of the economy and a broader index.

- As the firm has grown performance has lagged. Berkshire has underperformed by book value in 4 of the last 5 years and in 5 of the last 10 years.

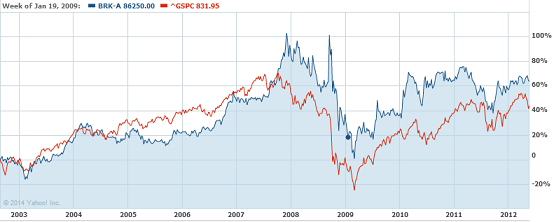

- When comparing the market performance the firm is starting to look more and more like a version of the S&P 500:

- On a risk adjusted basis, it would not be unreasonable to argue that Berkshire exposes you to performance that is similar to a broader index, but exposes you to substantially greater non-systematic risk.

Buffett shouldn’t be searching for someone to explain the bear case on Berkshire. He should be looking for someone to explain why anyone should continue to hold his firm’s stock relative to a broader index. Now, THAT would make for a fair and interesting discussion.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.