About a month ago I wrote a piece titled “Please Stop with the ‘Money Printing’ Madness”. The post describes how wrong it is to describe the various operations in previous years as “money printing” (whether it be QE or deficit spending). Yet this has been one of the dominant themes over the years.

Of course, the idea of “money printing” implies that inflation is likely to result at some point in the future. More money will chase more goods, etc. And this concept has been used repeatedly in recent years to justify specific portfolio positioning by investment managers. In brief, you short the USD relative to other currencies, you short US government bonds and you buy hard assets. In particular, these “money printing” proponents have been huge advocates of buying gold and silver.

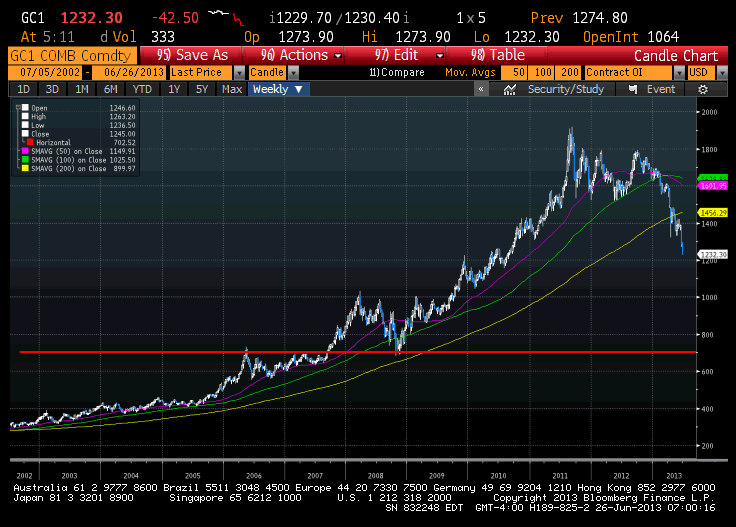

So, it’s interesting to ask, as gold and silver prices crumble, are we finally seeing more people come around to the idea that the “money printing” myths have been based on a false understanding? Will people finally stop referring to QE as “money printing”?

(Gold chart via Mark Dow)

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.