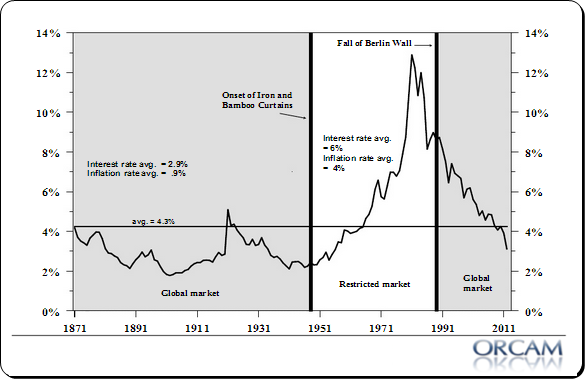

One thing I constantly hear is “interest rates only have one direction to go – UP!” There’s this myth that t-bond yields and interest rates in general just have to go higher. But history does not prove this at all. In fact, history tells quite a different story.

The chart below helps put things in perspective. Since 1871 US Treasury Bond yields have averaged 4.3%. Today’s rates of 2.8% are certainly lower than that, but not at record lows. We’re still about 1% off those levels seen at several points in the past 125 years.

It’s also interesting to note that the high rates of the 70’s are a substantial anomaly in the data. It looks like many are suffering from a case of recency bias here. And by recent, I do mean the 70’s. That’s not entirely inappropriate given the long duration of these bonds, but when one steps back and reviews the true long-term history of bond yields the current environment looks much more benign than most imply.

(Chart via Hoisington)

{kind=link}

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.