The news of an executive reshuffling at WealthFront comes at an interesting juncture for the Robo Advisory space. With growth slowing for some of the main players and more big names entering the game, it’s worth considering if we’ve seen peak robo advisor?

My view has always been the same – robo advisors are mostly a fancy interface implementing a low fee indexing strategy that amounts to little more than a target date mutual fund or some version of the Vanguard Tax Managed Balanced Fund. The only reason you would ever open a robo advisor account is if you are unaware of the fact that you’re buying something that already exists in a lower fee structure. You know, the same reason why people own trillions in closet index funds and hedge funds….sigh. I know I am harsh on issues like this, but I truly loath seeing high(er) management fees where you can buy something virtually identical for far less….

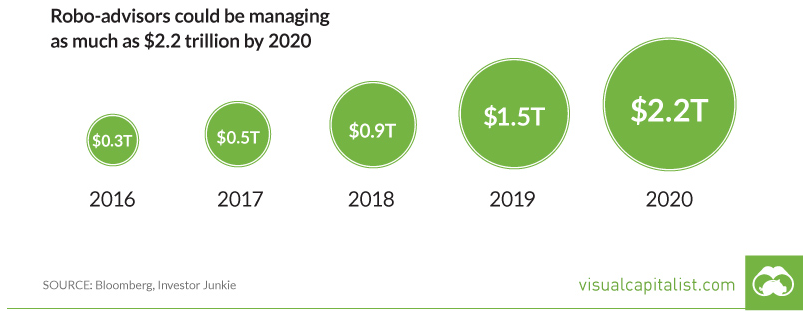

But we’re about to see some serious firepower enter the space as Merrill Lynch and Fidelity both enter the fray. These are firms, mind you, that I would argue have been behind some serious curves in the asset management space so their entry here might be more disconcerting than anything else. Still, they will drive huge amounts of assets into their products. So it’s not unreasonable to assume that the robo space will see trillions in assets under management by 2020. Good marketing and sheer manager size will drive the asset growth, if nothing else.

So no, this isn’t peak robo. But we’re definitely at a point where the space is incredibly saturated. I suspect that what we’ve seen here is a product wrapper that is packaged as a shinier looking version of a product that already exists. And as people realize that they’re just buying a tax managed target date fund with a bunch of extra fees added on they’ll close up these accounts and buy the real thing instead. As that trend reinforces itself it won’t spell doom for these players, but it will mute growth substantially just as we’ve seen across the entirety of the active management space which more and more people are realizing is little more than a version of something that exists in indexing form already.

NB – An addendum is probably appropriate here to put things in some perspective. Although I don’t see a lot of value in most robo services I am remiss in not saying that these are far superior services than so much of what’s on Wall Street these days. Many firms like closet indexing mutual funds are pure negative value adds to our economy. A low fee robo firm is at least providing a reasonably priced alternative with some degree of benefits depending on the client. So, my criticisms shouldn’t be overstated. When it comes to the “good guys” vs the “bad guys” on Wall Street I am more inclined to include the Robo services in the “good guy” camp. Sorry if I appeared overly critical….

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.