One of the hottest debates in economics today is about the topic of financial stability and whether the Federal Reserve and other policymakers should be concerned with trying to stabilize the financial markets at times. Many prominent economists argue vehemently that the Fed shouldn’t be concerned with such matters while many others argue that financial stability is a legitimate concern.

I think it’s rather clear that financial stability has become a growing area of concern for one simple reason – accessibility to financial markets has created an environment in which households are increasingly susceptible to financial market shocks. This makes the overall economy more sensitive to financial market shocks.

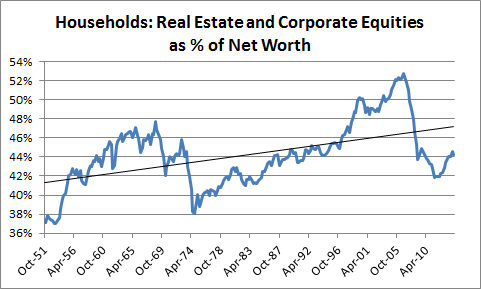

Here’s a simple chart showing the value of corporate equities and real estate as a percentage of hosuehold net worth going back to the post-war era:

There’s been a clear uptrend in these two markets as a percentage of household net worth primarily because ownership of both real estate and stocks has increased over time. This means that household balance sheets are increasingly comprised of relatively volatile asset classes. And that means that big shocks to these markets have an increasingly important impact on the overall economy.

Additionally, the household sector has become increasingly leveraged in the post-war era. Household debt as a percentage of net worth has increased from just 6% to over 16% in the last 60 years. It rose as high as 25% during the housing bubble. Add financial sector leverage on top of this and you have a private sector whose balance sheet is increasingly dependent on potentially volatile asset prices.

Of course, we have to understand the context within this debate. I agree that financial stability probably isn’t a legitimate reason to raise rates at present. I don’t think there are broad signs of financial instability. But I do think that this is something that the Fed and policymakers should try to be aware of because an economy with rising levels of volatile asset ownership could mean an economy that becomes increasingly fragile to shocks.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.