In a great piece over the weekend Josh Brown goes into some detail on the situation with Bill Gross leaving PIMCO. He asks the important question – what does an owner of the Total Return Fund do now that Gross is gone? I’m not going to answer that question, but I did think there was an important lesson in Josh’s post.

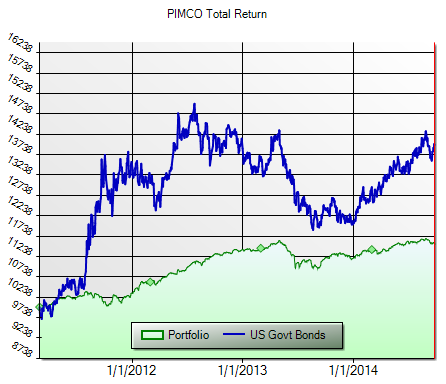

In 2011 Bill Gross, who had crushed the aggregate bond market by almost 2% per year before fees for 30 years, made one of the most vocal bets on interest rates that we’ve seen since the crisis. He was very worried about rising rates when QE ended. He asked “who will buy the bonds” in his March 2011 monthly letter and his bearish stance on T-bonds led him to reduce his allocation to T-bonds to zero.

I was very vocal about this view at the time because I believed Gross was misunderstanding the impact of QE. In fact, I thought a large portion of the field of finance and economics was misunderstanding the risks of QE, the “money printing”, etc because they weren’t properly understanding its operational reality. In essence, Gross was saying that interest rates would rise because QE was ending and the decline in rates due to QE would have to reverse. That is, of course, unless you don’t think QE had much of an impact on rates to begin with. If that was your belief and you thought that inflation would remain low (as I did) then there was really no rational reason to expect interest rates to surge following the end of QE2.

Of course, Gross ended up being wrong as rates actually fell after QE2 ended. The Total Return Fund went on to underperform the long bond by a huge margin  over the next 2 years and the very public call came under harsh scrutiny. Investors began to ask if Gross had lost his touch. And the fund flows reversed out of the fund began as quickly as they’d flooded in after 2008. As the years went by Gross appeared to never recover from the call and last week we learned that Gross was leaving the firm he founded.

over the next 2 years and the very public call came under harsh scrutiny. Investors began to ask if Gross had lost his touch. And the fund flows reversed out of the fund began as quickly as they’d flooded in after 2008. As the years went by Gross appeared to never recover from the call and last week we learned that Gross was leaving the firm he founded.

The interesting thing is not that Gross was a victim of bond market ignorance – he’s obviously a bond market genius, far more savvy than a chump like myself. but he was a victim of macro ignorance. The implementation of QE by the Fed had forced all market participants to take on a whole new set of understandings. And those who had a sound understanding of macroeconomics were better prepared to deal with the aftermath.

In my new book I outline 8 rules for picking an asset manager (see here). Rule 8 is ensuring that a fund manager has a sound understanding of the macro world. Misunderstanding the big picture creates tail risks in a portfolio because it means that fund manager exposes investors to the risk that he/she could dramatically misunderstand important macro events. And in a world where everything is becoming increasingly macro oriented (whether it’s Fed policy, dependence on global events, etc) you can’t afford to invest with asset allocators who don’t have a sound understanding of the macro environment.

Of course, understanding the world isn’t a guarantee of future performance. But I am a big believer in the idea that those with a superior understanding of macro dynamics will be better prepared to manage the risks that threaten investment performance. In other words, by having a superior understanding we can better understand what we know in addition to what we don’t know. And this ultimately helps you avoid the pitfalls that befell the PIMCO Total Return Fund.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

John Daschbach

There are a lot of working parts in the whole macro economic picture. I don’t think anyone precisely understands QE. Among economists there remains disagreement about QE depending upon one’s primary set of paradigms, and even among those who predicted it wouldn’t have much impact on Tsy yields there are different paradigms driving the arguments.

I would consider a big part of your call to be based in something that you consider macro economics (balance sheet recession) and that others might consider behavioral economics and perhaps rational expectations (people would expand their credit liabilities if future prospects looked good). Are these the same or different?

Another part of the macro picture is the fiscal contraction which plays into this. In this sense the fiscal conditions have both what you consider macro economic factors and conditions that many economists consider rational expectation or behavioral.

Some argue (you have a bit) that overall we haven’t had austerity and significant fiscal contraction. This is true. But when you break it down along a behavioral or RE paradigm it looks different. Transfer payments increased and government employment decreased. A behavioral view which goes along with the balance sheet recession view, would argue that people getting transfer payments and seeing the job losses and anticipating poor prospects would pay down their balance sheets.

I think that some respected right wing economists, like John B. Taylor, failed to connect all the dots, which is surprising because he also advocates for long term tax reductions and argues that short term tax reductions don’t work because of rational expectations (makes sense).

It’s unlikely QE would have been used at all if government employment had not dropped so significantly.

I would summarize your call as consisting of a set of paradigms you consider important. But it’s not all macro. The asset swap concept is, I would argue, a pure macro financial micro founded argument, and almost certainly correct. The balance sheet recession is again part of a macro financial micro founded view but it’s not a simple macro argument. The portfolio rebalancing impact of QE on asset prices is more of an EMH macro economic view.

In other words, every picks and chooses a set of primary basis vectors in the complex space of economics. Nobody gets it correct every time, and it appears those who do best combine a wide range of paradigms, from micro to macro.

Andrea

YES!

I am a firm believer that understanding the macro picture at a superior level (as in: NOT textbook classical macro) is key to a) superior returns and b) superior risk management.

At a minimum, it will help to admit when something is likely to be more complicated that the naive economic view presented by mainstream economists, most of whom are glorified salespeople for their own institution.

I have been making this point in my presentations quite frequently, but it is a hard concept to push to an audience who is very much captive to the conventional wisdom of things.

DevilsDictionaries.com

This is one of the most valuable articles I’ve read recently.

jswede

Gross has been so very average in the last 5+ years, and now further anecdotes about his god-like complex…

possible Gundlach will see more of the PIMCO outflows than Janus.

quaking

The operational reality is that the central banks will buy the bonds — T-bonds, mortgage bonds, soon-enough student loan bonds. So whoever can navigate that reality will be successful. … It looks like a difficult reality, though — low growth, low interest rates and the danger that if you keep adding money/debt to the system without sparking growth that we are entering uncharted waters.

tealeaves

Japan has 10 years plus on the US. And Europe is just behind them.

Simon

“Macro” has always been an important driver in FX and rates markets, somewhat less so in credit markets and really only became de rigueur in equity markets during the 2009-2013 period. A period where fear of systemic failure meant macro events controlled risk-on/risk-off sentiment like a lightswitch.

To quote the great Peter Lynch: “If you spend 13 minutes a year analysing economics, you’ve wasted 10 minutes”.

connie hawkins

gross was not wrong, he was just early. gross failed to anticipate twist, qe3, etc, etc.

Russ

Pimco’s biggest challenge isn’t recovering from Gross’s departure, but continuing to try to manage an asset base that far exceeds many of their product’s true capacity. As an industry, we have too many assets gathered among too few mangers, and their ability to add alpha is severely damaged by their sheer size.